Estate and Capital Gains Taxes in Washington State

Washington’s Engrossed Senate Substitute Bill 5813 (“ESSB 5813”) became the law of Washington on May 20, 2025. ESSB 5813 provides significant legal changes to Washington’s tax system. Understanding what’s in play with the new law is only half the battle. The real challenge — and opportunity — is how you respond to estate and capital gains taxes in Washington State. Whether you work with a trusted advisor or chart your path, now is the time to assess your strategy and take thoughtful action.

What’s included in ESSB 5813?

So, what are the tax changes in the bill, and how will they impact you?

1. Washington capital gains tax rate increases

- Prior law:

- A 7% capital gains tax applies to Washington-based long-term gains above $270,000 (adjusted for inflation).

- Retroactive to January 1, 2025:

- 7% tax on gains above $270,000 (adjusted for inflation) up to $1 million

- 9.9% tax on gains above $1 million

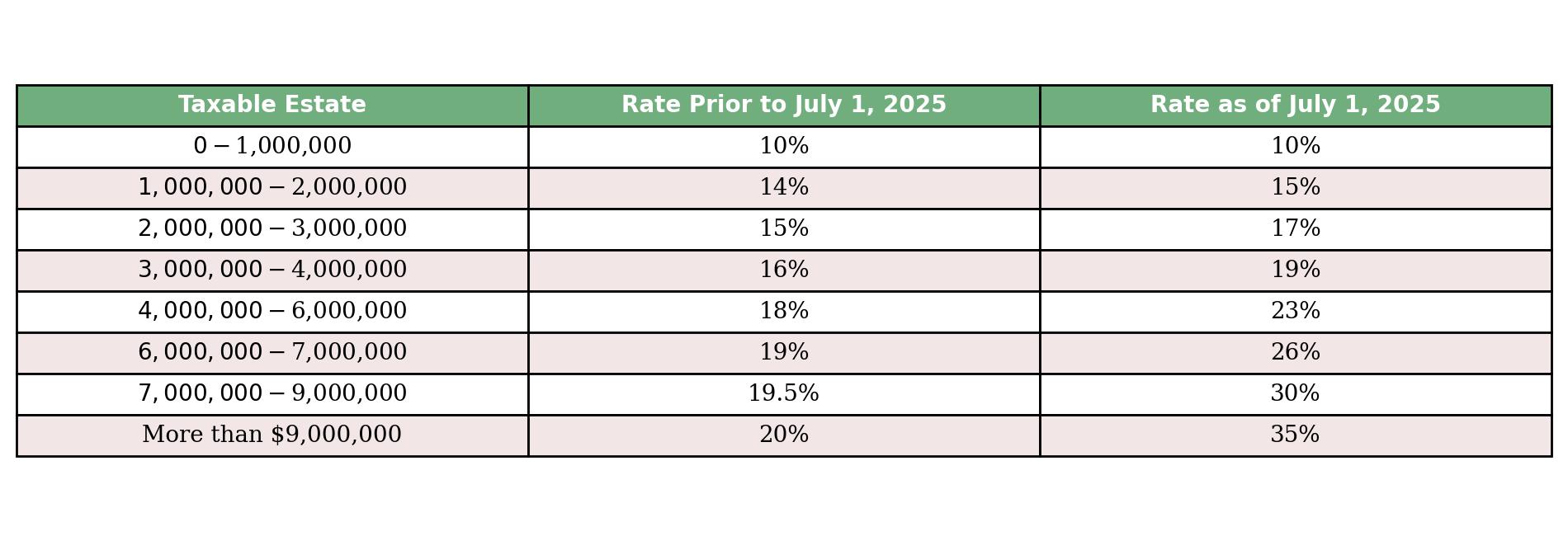

2. Washington estate tax changes

- Exemption increase:

- From $2.193 million to $3 million, with inflation indexing restored. Effective July 1, 2025.

- Rate increases:

- For estates valued over $4 million, rates rise significantly.

Reference: https://dor.wa.gov/taxes-rates/other-taxes/estate-tax-tables

Reference: https://dor.wa.gov/taxes-rates/other-taxes/estate-tax-tables

Planning with intention: How to respond proactively

Tax changes in ESSB 5813 can create urgency, but it’s best to meet the moment with clarity, not haste. Responding with intention means stepping back, understanding the implications of your whole financial life, and making decisions that reflect your goals and values, not just the tax code.

Navigate these changes with the following:

1. Redesign your estate plan as a legacy plan

Raising the exemption helps, but estates above $4 million face significantly steeper taxes. Now is the time to revisit estate strategies — from trusts to charitable giving to insurance planning — to preserve wealth and reflect the legacy you want to leave behind.

Evaluate gifting strategies, family trusts, philanthropic vehicles (like Donor-Advised Funds or Private Foundations), and life insurance overlays as tools for tax efficiency and to pass on values alongside assets.

2. Evaluate relocation with eyes wide open

Some may consider leaving Washington for lower-tax jurisdictions. But financial efficiency isn’t the only metric. Is that move aligned with your family life, community, or impact goals?

Run jurisdictional comparisons that don’t just weigh dollars but consider lifestyle, support networks, and intention. Then, craft a plan that supports your long-term happiness, not just your short-term tax bill.

3. Merge income and estate strategy

In an environment of rising taxes, how you give, spend, invest, and transfer wealth becomes increasingly interconnected. A siloed strategy can mean missed opportunities and avoidable tax costs.

Coordinate tax-smart withdrawal strategies, Roth conversions, and charitable gifting with long-term estate strategies. A well-sequenced plan could reduce lifetime taxes while empowering your impact.

What happens next?

With ESSB 5813, Washington has signaled a long-term shift in how it taxes high earners and high-value estates. If you’re not planning, you may find yourself reacting later.

At Brighton Jones, our Personal CFO teams are already modeling scenarios and crafting tailored strategies to help clients take proactive, values-aligned action. Whether it’s evaluating potential liquidity events, rethinking your estate structure, or balancing tax efficiency with life decisions, we’re here to help you stay aligned and ahead.

This content is for informational and educational purposes only and should not be construed as individualized advice or a recommendation for any specific product, strategy, or course of action. Brighton Jones, its affiliates, and employees do not provide personalized investment, financial, tax, or legal advice through this communication. This material is not intended to, and does not, create a fiduciary relationship under ERISA or any other applicable law. For individualized advice tailored to your specific circumstances, please consult with your adviser.